Easy PMI Removal: Stop Paying the Bank’s Insurance.

If you bought a home in the DC Metro area with less than 20% down, you are likely burning $150 to $400+ every single month on Private Mortgage Insurance (PMI).

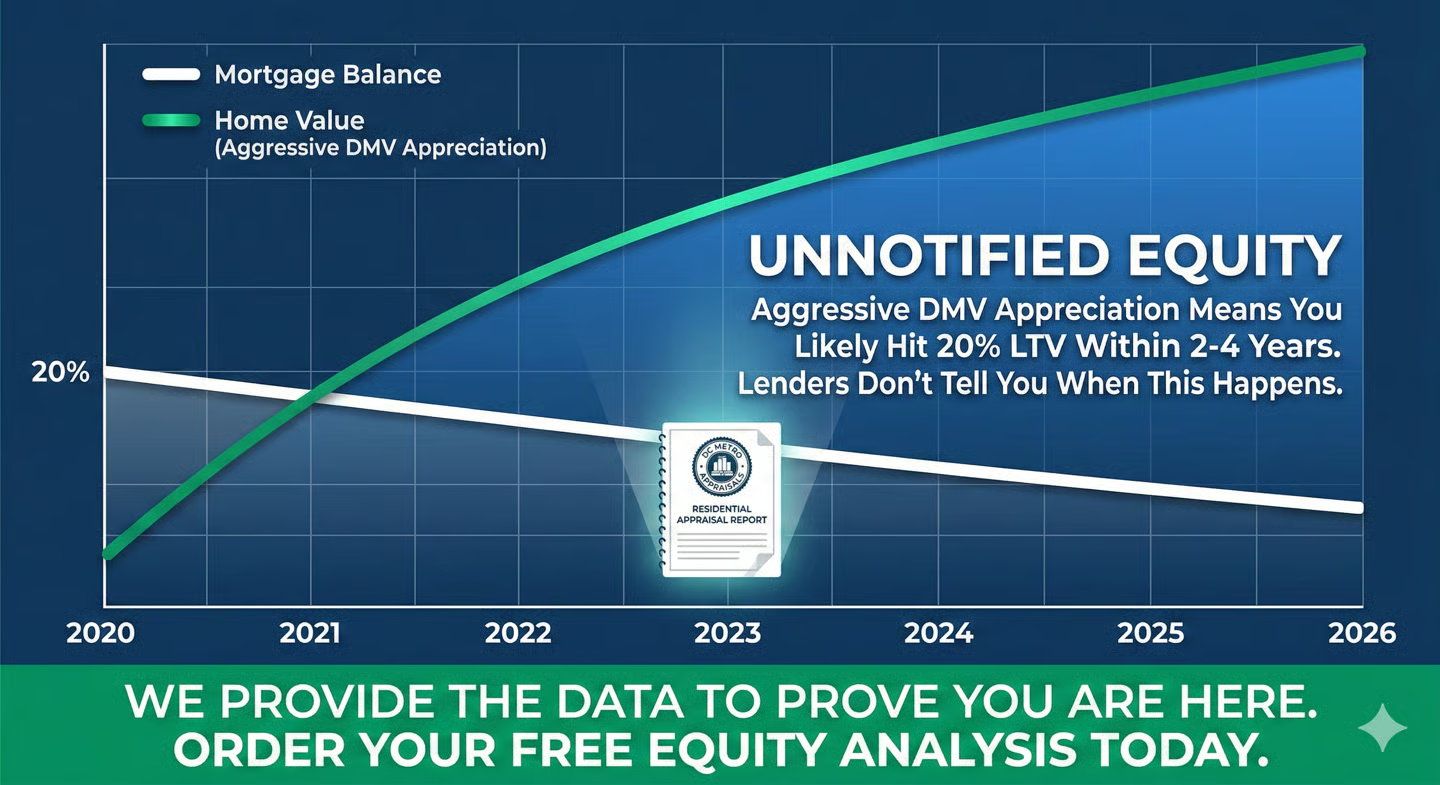

Here is what your mortgage servicer isn't telling you: You do not have to wait 10 years to pay down your loan to get rid of PMI. Because properties in Northern Virginia, Washington D.C., and Maryland appreciate so aggressively, you can use your home's new market value to force the bank to drop the fee.

The "Seasoning" Rules: When Can You Drop It?

Banks have strict timelines called "seasoning periods." Here is exactly what you need to know before you try to drop your PMI:

* The 2-Year Rule: Conventional loans typically require a seasoning period of two years before you can request to remove PMI based on a new appraisal and increased home value. (Note: If you have made massive structural renovations, some lenders will waive this 2-year wait).

* Under 5 Years Owned: If you have owned the home for at least two years but less than five years, lenders often require the new appraisal to show a Loan-to-Value (LTV) ratio of 75% or less.

My Exclusive "Risk-Free" PMI Equity Check

Most homeowners hesitate to order an appraisal because they don't know if they meet those strict 75% or 80% LTV rules. I have eliminated that risk.

Before you pay for an appraisal, I offer a 100% Free PMI Equity Analysis.

You give me your address and your current loan amount. I will pull the raw, recent sales data for your specific neighborhood and send it to you. You can look at what similar homes are actually selling for and decide for yourself if you want to move forward. You only pay for an appraisal when you are confident the local data makes sense.

The Math is a No-Brainer:

* The Cost: A one-time Certified PMI Removal Appraisal for $645.

* The Return: Dropping a $250/month PMI payment saves you $3,000 every single year. This appraisal pays for itself in just over two months. After that, thousands of dollars stay in your pocket.

The "Easy" 3-Step PMI Removal Process:

* Call your loan servicer: Ask them for their specific PMI removal requirements based on "current market value" so you know exactly what LTV target you need to hit.

* Get Your Free Equity Check: Fill out the secure form below. I will run the neighborhood data in minutes to see if you have a strong case.

* Order the Appraisal & Save: If the data looks good, I will conduct a full interior Professional Property Walkthrough and deliver a legally defensible, certified appraisal in 5 to 7 days. Hand my report to your lender and watch your monthly payment drop.

Stop throwing your equity in the trash. Fill out the form below to start your Free PMI Removal Analysis today!

Please include in the Message/Notes box:

* Your Name, Email, and Phone Number

* Your Property Address

* Your Current Loan Amount (So I can run your LTV data)

* Recent Improvements (Briefly list any major updates, renovations, or additions you have made since purchasing the properly)